Web3 Funding: April in numbers

Please like and subscribe!

We are 50 days into lockdown in the UK and the economy on pause is taking its toll on the tech and startup world. Continuing the tradition I am looking into the fundraising data for April to get a comprehensive view of the state of web3. I am doing this every month to see how the true effect of COVID-19 unravels in the web3 world in near real time.

Source: Crunchbase

April saw 32 deals at nearly $50m. We’re 50% down from last month (excl Bakkt raise).

Last month we were more or less on par with March 2019. Now we're half from there. Crypto winter isn't over and is not entirely immune to macro economic trends as majority of the deals are done in equity. We also had more startups disclose their rounds. Positive news is we saw two instances of token-based rounds and rumours about some investors being more interested in tokens than equity.

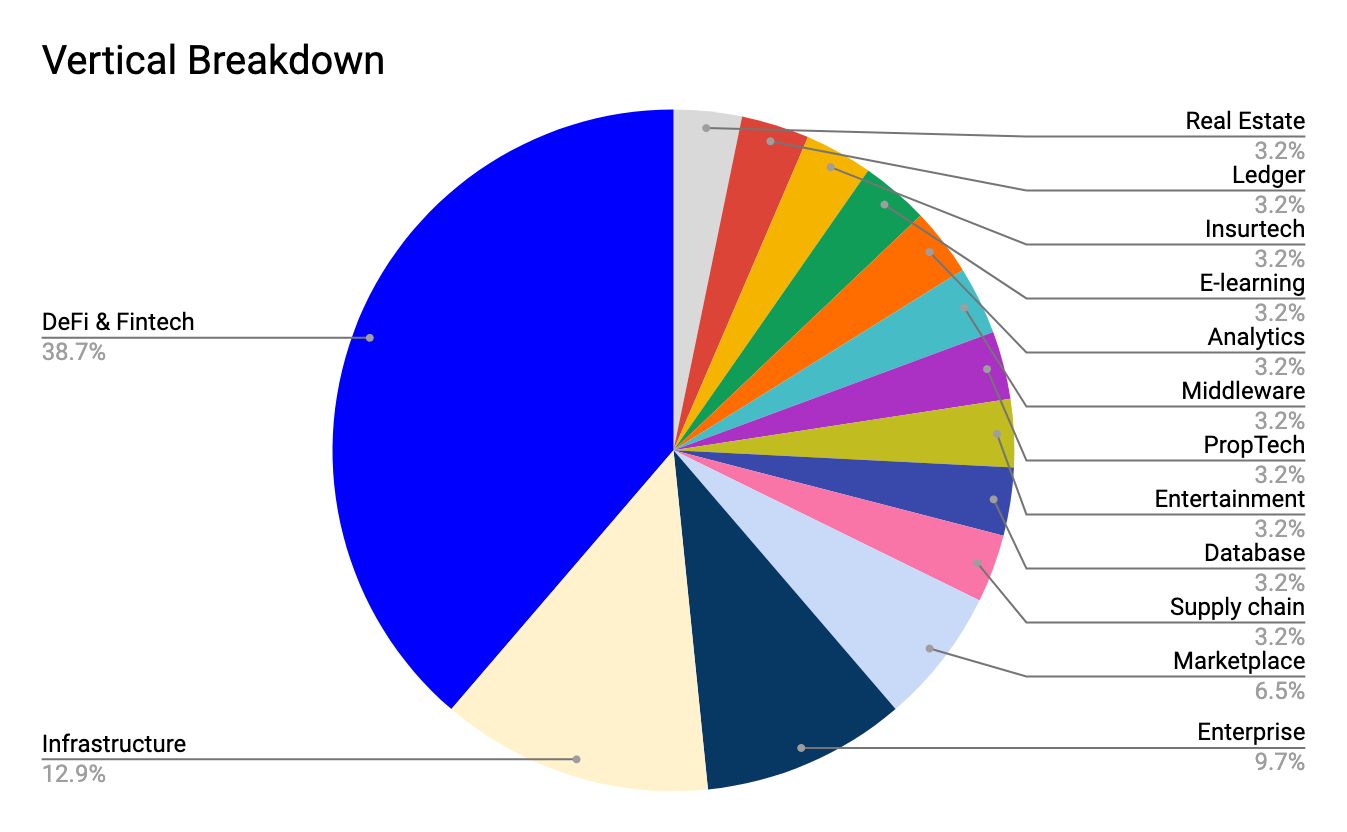

Over a third of the deals in April were once again in DeFi & Fintech.

Source: Crunchbase

DeFi & Fintech also attracted over half of the funding with almost $30m committed.

Most companies in the category did not disclose funding so this is one reason why the number is so significantly low. We still cannot declare this to be a true effect from the pandemic as most deals have been in months-long negotiations. Those who did range between $185k to $7.7m and $14m. The startups raised mostly seed or seed extensions with Crypto Finance AG getting to Series B.

If your startup closed in April and is not on the list, email me! Same goes if you are on the list and wish to disclose round size - only aggregated data is published.

Source: Crunchbase

The most common round in April was seed.

Equity seed funding proved to be the most attractive stage in April 2020. Pre-seeds were nowhere to be found continuing the trend of investors willing to wait and pay a higher price to de-risk the investment by seeing some early market and product validation. Crypto Finance AG closed their Series B which was one of few later stage rounds. Props and Keep collected decent rounds via tokens and Neptune Dash managed to score post-IPO funding (IPO’d 2018 in Canada). Congrats to team Portis for the Shapeshift acquisition!

The most active Fintech/DeFi category is lending.

Source: Crunchbase

Cadence, Atomic Loans and dForce all raised seed. dForce’s announcement was kind of drowned in the news about the flash loans exploit but nevertheless they had Multicoin, CMB Capital and Huobi trust them with $1.5m. Exploits and hacks are part of the risks in early stage DeFi that most investors should be prepared to go through, especially in novel lending solutions.

Followed by banking, exchanges and trading. Asset management, middleware and payments are trailing with 1 deal each.

The trends within DeFi & Fintech shifted since last month with more emphasis on lending and less on exchanges and payments. Financial middleware is a fairly new exciting category where investors and founders see potential for enabling a bigger market.

Startups:

Banking: Bitpanda, DeFiner

Exchanges: tZero, LGO Group

Trading: Set Labs, Dsdaq

Asset management: Crypto Finance AG

Financial middleware: Sila Money

Payments: Pie People

A bit over a tenth of all funded startups in April are building in Infrastructure.

Source: Crunchbase

Infrastructure here includes node operators, platforms for processing rewards and private data interactions, marketplace infrastructure.

Startups:

Neptune Dash - nodes

VikRee - marketplaces

Props - rewards

Keep - private data

Followed by almost a tenth being multi-purpose consultancies enabling enterprise adoption of DLT.

The pandemic made it clear for enterprises that to survive they need to speed up their digital transformations affecting various parts of their businesses. From Insurance and Financial Services companies dealing with outdated workflows to supply chains being interrupted by the human factor and a demand shock. The enterprises are speeding up their research into automation and connected devices.

If you are building in machine to machine, reach out to me!

Decentralised tech is poised to follow as many realise effective machine-to-machine communication is still a problem. We may have to wait for a year or two before enterprises start committing due to long sales cycles. Startups like Fetch.AI (OV investment) have been building for this moment in the past few years and are ready to jump in.

Startups:

Applied Blockchain

Grainer

Yun Qu Technologies

Underrepresented categories were marketplace, real estate, supply chain, databases, entertainment, proptech, middleware, analytics, e-learning, insurtech, distributed ledgers.

The focus here shifted slightly, but the categories are still pretty much the same with the additions in entertainment, proptech, e-learning and insurtech. Middleware saw less companies closing but from what I am seeing at pre-seed and angel level we’ll see some rounds getting closed in the next few months.

Startups:

Marketplace: Lootmart, Walzay

Real estate - DomiDocs

Supply chain - Minespider

Databases - GeoDB

Entertainment - Big Couch

Proptech - EHAB

Middleware - Portis

Analytics - Skew.

E-learning - Box Media

Insurtech - Sprout.ai

Distributed ledgers - Asensys

Blockchain gaming received loads of media attention in March but no companies closed funding in April.

Gaming is a difficult business and adding another layer of complexity is not going to speed up the process. Games appealing to the end user are driven by content first and tech like blockchain second and service businesses have a limited upside apart from a few ca ses. What I’ve been seeing in crypto is that many go tech first and content second, so excited about some of the up and coming studios' approaches. Certain infrastructure solutions will be interesting, especially if coming within the industry. If building something like this, shout out!

https://twitter.com/litcapital/status/1258832487054180353?s=20

Companies came from all over the world.

North America (US & Canada) saw almost half of the deals that closed in April 2020. The UK is trailing behind with 20% and Europe has a little bit above a tenth similarly to Asia. Israel and the Middle East only saw a deal each.

Part of the reasons behind this split could be funding available. The US has more private funding available and the UK and Europe have multiple grant programs for innovation alongside some private capital from institutions and angels. A lot of early stage investors will be moving towards late seed as many need to de-risk to an extent and series A's will be difficult to close. I am seeing a lot of pre-seed stage companies in Europe that will take at least a couple of months to get investor ready.

Some investors are still doing deals and others chose to pause for various reasons.

Some investors want to take time and evaluate the market, others are more certain in their theses more than ever. One thing valid for everybody is the super hands on work on portfolio companies is now easing up a little and freeing time on their calendars.

https://twitter.com/auren/status/1257691742087733248?s=20

VCs have exposure to different verticals, technologies and stages. Some will be doing better than others. All founders should keep this in mind based on portfolio. Now it's more important than ever to profile partners at your target funds and personalise your reach out.

Web3 Funding: April in numbersNimble Ventures, QBN Capital, Startup Funding Club did multiple deals. Consensys, Multicoin, Paradigm, Huobi Capital, Fenbushi Capital, Coinbase Ventures are amongst the crypto VCs who closed deals at seed and beyond in April. This is not a reliable indicator they’ll still be committing but there’s a good chance.

For data requests, use of graphics or quotes, reach out to ana [at] ana [dot] vc. Allow for slow response as navigating the current messy world takes up most of my time!