Web3 Funding: March in numbers

Web3 Funding: March in numbers

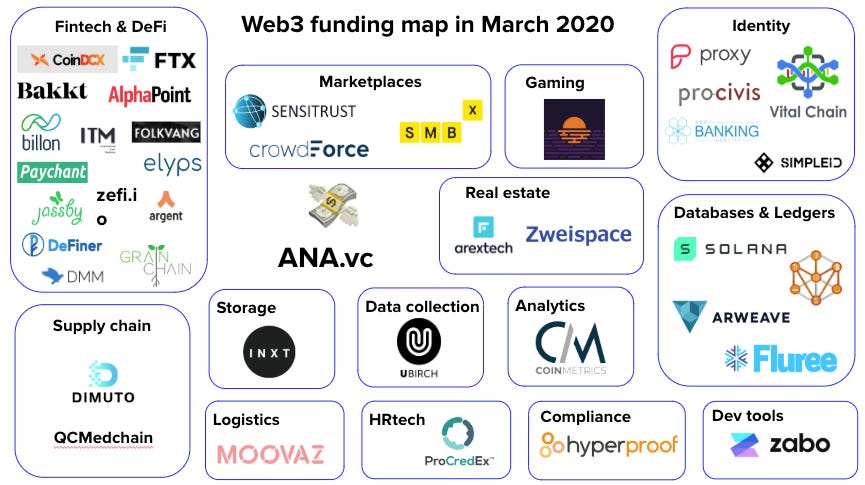

Who raised and which markets attracted the most

March is the weirdest month so far with events affecting both our personal and professional lives. COVID-19 didn’t skip startup and VC life either. I’ve been following VC twitter for a while now and there’s been loads of talk about “business as usual”. Well, the truth is we cannot be further from business as usual. We’re back where we started a year ago.

I will be looking into the March data to get a comprehensive view of the state of funding and will be doing this every month to see how the true effect of COVID-19 unravels in the web3 world.

March saw 39 deals with real activity at $117m.

The total activity is at $417m with Bakkt's $300m mega round. The real activity for the other 38 deals was at $117m across all stages.

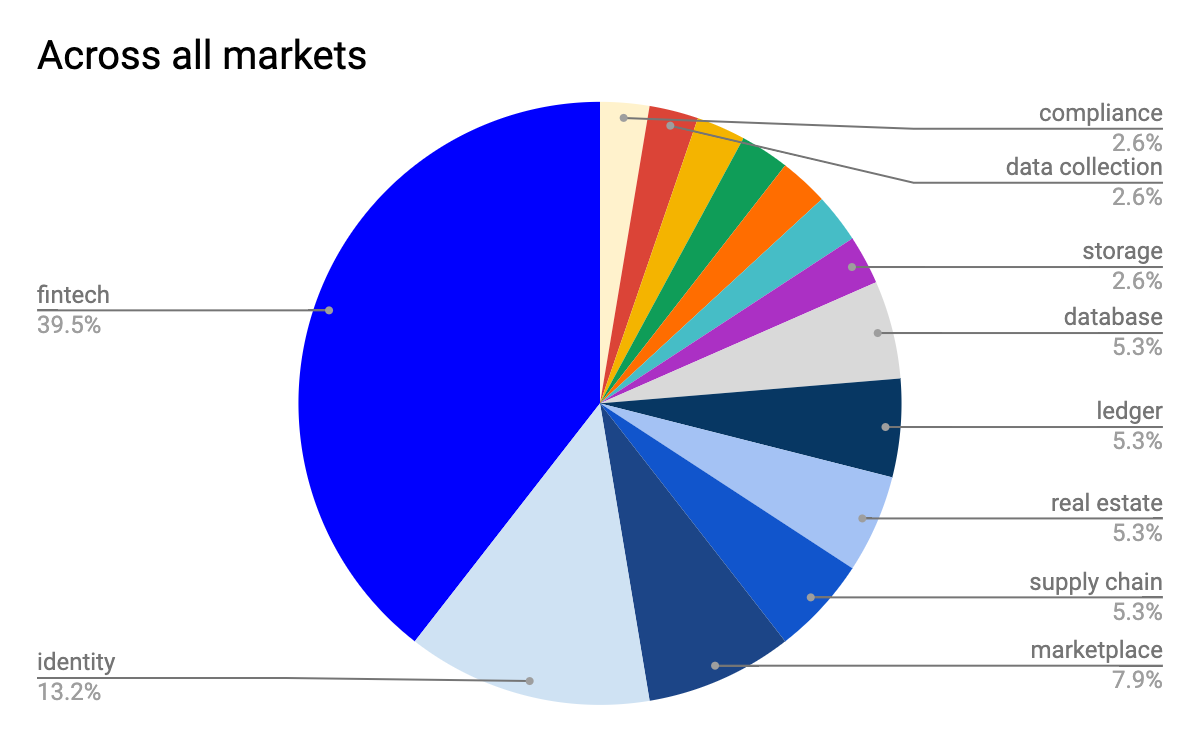

Over a third of the deals in March were in Fintech & DeFi.

However, identity attracted most of the money with $43m in total funding with Fintech & DeFi attracting $41m.

(excluding Bakkt’s round)

The median round in Fintech / DeFi was $5m with seed ranging between $150k and $1.8m. The quality is still a concern amongst the investor circles. The good news is that it has been improving in the past year and we will get to a point where a large pool of well operated high growth businesses will become a thing in web3.

Self-sovereign identity (SSI) is the pinnacle of digital identity. The importance of it is evident seeing the category collected most of the $$ available for web3 startups and attracted a great pool of tier 1 investors.

The most common round in March was seed.

Seed funding proved to be the most attractive stage in March 2020. Pre-seeds only booked 4 deals meaning that investors are willing to pay a higher price and wait longer to de-risk the investment by seeing some early market and product validation. Gone are the days of paper projects collecting millions.

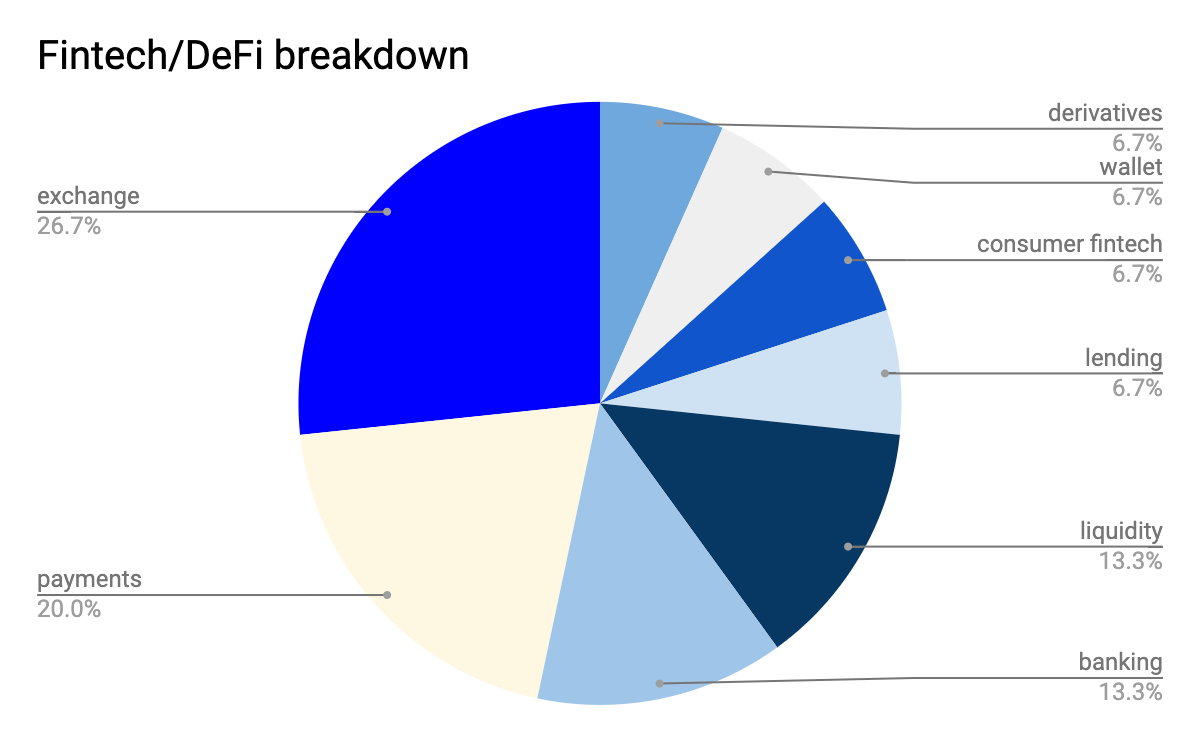

The most active Fintech/DeFi category is exchanges.

CoinDCX, FTX exchange, Bakkt, Grainchain all raised growth capital with Bakkt attracting a $300m round. Exchanges are a lucrative business as the trading fees will keep going regardless of where the market is swinging. The biggest challenge now seems to be differentiation and attracting volumes. It is a capital intensive business, so not surprised by the amount of series A+ capital going into it.

Followed by payments, liquidity and banking. Lending, derivatives, wallets, consumer Fintech are trailing with 1 deal each.

Seed: DeFiner, Paychant, ITM, Zefi, Elyps, Folkvang, DeFi Money Market

Series A: Billon Group, Alphapoint, Argent, Jassby

DeFi still attracts mostly seed and some series A funding meaning it is still largely pre-product-market fit. Although still wrestling with using decentralised tech and appealing to a large user base, some of the projects have real potential to crack the code.

A tenth of all funded startups built in Identity.

Pre-Seed: SimpleID

Venture Series Unknown: NewBanking ApS, Vital Chain

Corporate Round: Procivis

Series B: Proxy

Self-sovereign identity is an interesting category with massive potential. The greatest challenge will be to balance regulation, security and ease-of-use. For some that will mean cutting off the end-user interaction with the product and selling directly to the developers. For others, it may take longer time to market for dealing with regulators to get access to the end-user data like passports, driving licenses, professional credentials, etc.

Followed by marketplaces, real estate, supply chain, database and distributed ledgers.

Marketplace: Sensitrust, Crowdforce, SMBX (seed)

Real estate: Arextech (pre-seed), Zweispace

Supply chain: DiMuto, QCMedchain (Grant)

Database: Fluree (seed), Arweave (seed)

Distributed ledgers: Solana (ICO)

Underrepresented categories were data collection, logistics, storage, compliance, HRtech, gaming, analytics, dev tools.

Data Collection: Ubirch - series C

Logistics: Moovaz - series A

HRtech: Professional Credentials Exchange - seed

Gaming: Horizon Blockchain Games - seed

Analytics: Coin Metrics - series A

Dev tools: Zabo - seed

Overall these categories compete with web2 startups, so raising a series A+ is quite impressive. It means they have cracked the way to use decentralised tech and still get the users and the revenue.

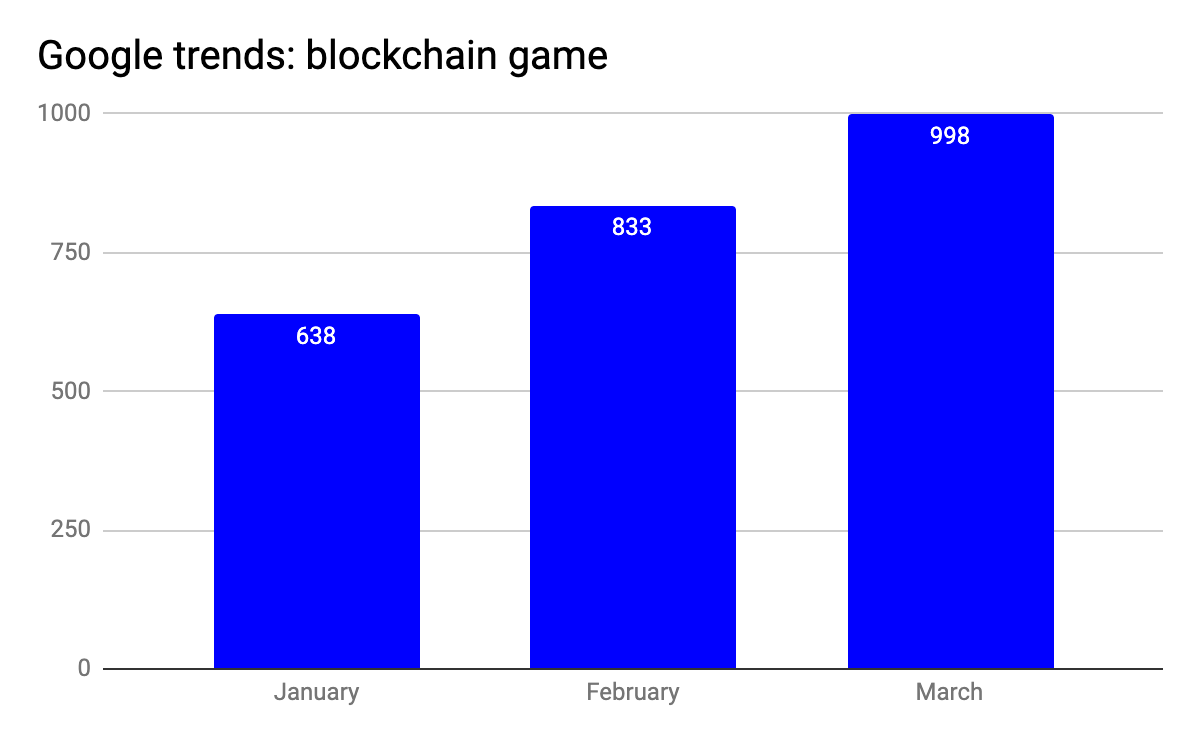

Blockchain gaming and analytics have received quite a bit of media attention in March, but lagging to be represented in VC-funded startups.

The trends for blockchain games showed increased interest in the topic, however, this hasn’t translated into as many deals with one startup rounding up funding in the category.

Investors were from a diverse base with a lot of ‘traditional’ VCs taking part in the industry.

Bain, Kleiner Perkins, Firstminute capital, Creandum, Index Ventures committed to deals across DeFi, identity and gaming.

Fun fact: in March, Y Combinator, Coinbase Ventures, DCG and Medici were the most active “crypto” investors each participating in 2 to 3 deals.

Pre-seed startups only had 5 deals with known deals collecting $900k.

If you’re building a pre-seed web3 company, I want to hear from you! We, at Outlier Ventures, are on a mission to fund the best founders. With that in mind, we are running the applications for our Base Camp accelerator until 17 April. It is a virtual-first bespoke program with residency in London and Berlin. Find out more here.

I will be releasing a list of startups for every market category with some analysis for all 39 deals. One category a day.

For data requests, use of graphics or quotes, reach out to ana [at] ana [dot] vc. Allow for slow response as navigating the current messy world takes up most of my time.